At the Vivensa Foundation, we believe that how we do what we do is as important as what we do. We place a lot of importance on our key values of being responsive, inclusive, trustworthy, long-term thinkers, collaborative and impact-intentional – and we expect our partners and award-holders to do the same.

We wanted to ensure the asset managers we work with, and their underlying portfolio companies, were aligned with our key values too. Chief Investment Officer, Andrew Gnaneswaran, explains: “Our aim is to use our £170m endowment in ways that enable us to do more for our mission.”

Initially, we were aiming to find a way to assess the impact of our investment portfolio. However, measuring impact in a consistent and robust manner presented a significant challenge. And particularly across a broad investment portfolio consisting of thousands of underlying companies, covering a variety of sectors, business models and geographical areas. So, we moved from seeking to understand the impact on people and planet of the investments in our portfolio, to building a values framework. This would help us understand how aligned the values of the investment managers and those of the underlying investments were with our own.

Understanding the values of our asset managers

Like many trusts and foundations, we don’t actively choose which companies to invest in. We choose which asset managers to partner with, and they take ownership of selecting the underlying companies in which their fund invests. But it’s these portfolio companies – over 2,000 in our case – whose business activities have positive and negative impacts on people and planet. We wanted to create a framework that allowed us to understand the values of the asset managers we work with, but also how those values are represented in the companies they invest in.

To start, we worked through our key values, describing what they mean in an investment context. Then we looked at how we might assess them, finding proxies to indicate a particular value or behaviour. For example, one of our key values is ‘long-term thinkers.’ So from an investment partner, we would want them to articulate a strategy that considers long-term risk and return. Therefore, we’d expect to see a low turnover of portfolio holdings.

Initially we thought about conducting this exercise in-house, but as the scale of the project became clear, we sought to bring in the expertise of a third-party. We needed help both to design the framework and to collect the metrics needed to perform the assessment. We decided to partner with Tribe Impact Capital – an impact-focused wealth manager – due to their experience in supporting clients to adopt investment approaches that align to their values. Tribe had existing approaches for assessing the impact credentials of asset managers and fund strategies. However, they wanted to work with us to develop a more bespoke framework that would help capture an analysis at both the asset manager and underlying portfolio company level.

Choosing an assessment framework

We looked at different options when we were choosing an assessment framework. The lowest cost and quickest approach was to rely on self-reported assessments. This would involve asking our asset managers some questions and trusting them to respond honestly. An alternative option was to utilise existing third-party frameworks, but these one-size-fits-all solutions weren’t based around our values. We looked at accessing publicly available data sets and layering multiple frameworks together to see if that could meet our needs. The final option was a fully bespoke model, where we’d gather independently obtained data. This could be commissioning someone to do a year’s worth of desk research and fact-checking. It was certainly the most rigorous choice, but also the most costly and time and resource-intensive.

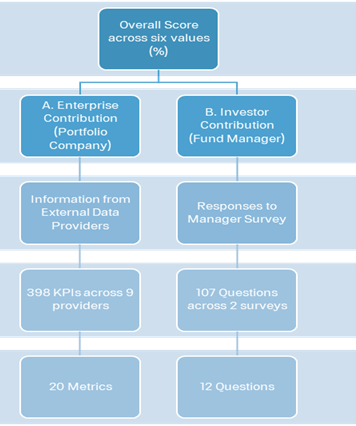

We ended up taking a hybrid approach. We conducted self-reported assessments at asset manager level, but at portfolio company level we utilised publicly available data sets to get a more robust picture. The survey asked our asset managers 100+ questions and their responses were analysed and aggregated to score their values-alignment. At the portfolio company level we picked nearly 400 data points from nine data providers. We ultimately distilled that down to 20 metrics, which were used to inform the scoring of each company in our portfolio.

How we measured our key values

Here’s an example of how we measured one of our key values, ‘inclusivity’, at asset manager level. We asked the managers if they had an EDI policy in place. If they said yes, they scored 100%. If they said no, we scored them 0%. We didn’t verify what they were saying – we had to trust their word. It was trickier to look at inclusivity at portfolio company level, as there is little publicly available data around class, education or ethnic diversity. We had to use gender as a proxy of diversity and inclusivity, so we looked into percentage of females on the Board as an indicator. That was the only readily available metric disclosed by the majority of portfolio companies.

We measured how aligned each manager was to our values, versus how aligned the sum of their portfolio companies were. Each company was scored, then the value of assets allocated to each company would weight the score. For example, the asset manager might be invested in an ethical, well-aligned company but it may only represent 1% of their portfolio.

This illustrates how difficult the exercise is, in practice, owing to the paucity of reliable data. We decided, though, that we needed a place to start. And the very act of asking for the data – and repeating those asks over time – would demonstrate to asset managers how serious we are. And in time, they will improve their data collection.

The final output

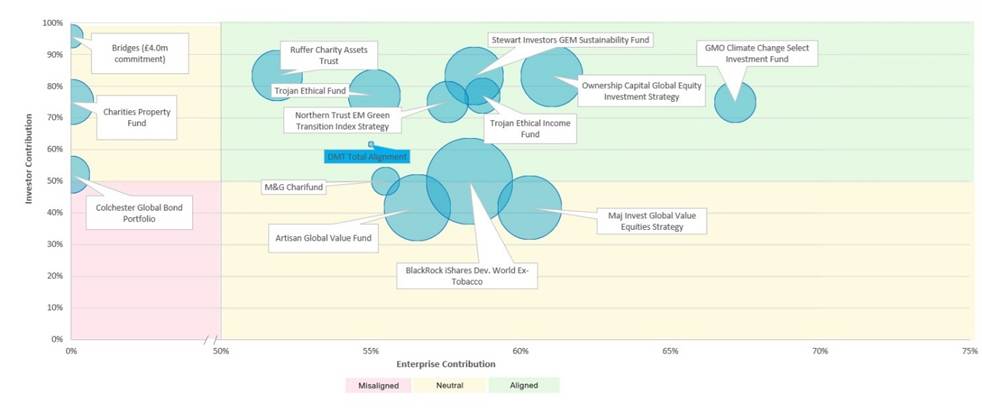

The assessment output places each investment into one of three categories: Misaligned, Neutral or Aligned.

There is a lot of detailed work underpinning the framework. It has given us a useful lens through which to look at proposals from new asset managers and to select new investments in future years. It has already helped inform and influence some of the investment decisions we have taken over the last year. These include divesting from Artisan, M&G Charifund and BlackRock.

Chief Executive, Susan Kay, says: “Some trusts and foundations are a bit further on than us in their investment practice. But, certainly from my conversations with peers, it seems that the majority are still at the stage of having conversations with their Boards, but not knowing how to progress. For us, this exercise has been enormously useful in growing our Board’s understanding of the regulatory developments in this area and their thinking on how our investment portfolio can be a major contributor to achieving our mission. I think it’s really sharpened up our strategic thinking and governance practices.”

__________________________________________________________________________________

Read our top five tips for developing a values-based framework for investment, which we hope will help others move from theory to practice.

You might also be interested to read this conversation with our Chief Executive Susan Kay and Chief Investment Officer Andrew Gnaneswaran, in which they reflect on our journey to becoming an impact-intentional investor.